Adele's 30 was Sony Music's biggest-selling record in its past fiscal year. But should the likes of Spotify and its rivals pay more for her music than 'flotsam and jetsam'?

Welcome to the latest episode of Talking Trends, the weekly podcast from Music Business Worldwide (MBW) – where we go deep behind the headlines of news stories affecting the entertainment industry. Talking Trends is supported by Voly Music.

In this episode, MBW founder Tim Ingham discusses the market share threat that the major record companies currently face on Spotify from DIY distribution platforms – and the millions of independent artists they service.

As music from these independent artists swamps streaming services, the majors’ refusal to allow the music they distribute to fall under a certain perceived quality threshold limits their ability to compete on volume / scale with the likes of DistroKid.

Ingham theorizes that the majors may soon pressure Spotify to pay out higher royalties for ‘quality’ or ‘premium’ artists – especially those who attract subscribers to its service – versus the tens of thousands of tracks uploaded to streaming services daily.

We hear from Rob Stringer, Chairman of Sony Music Group, who last week told investors that Sony has widened its own distribution net – via The Orchard and AWAL – to work with more independent acts, and counteract the market-share erosion created by DIY distribution.

However, Stringer noted that a proportion of this DIY-distributed music isn’t of a good enough quality to be considered anything more than “flotsam and jetsam”.

You can read an abridged transcript of this episode of MBW’s Talking Trends, complete with illustrative chart/s, below.

Subsequent to publishing that story, I had a meeting with the founder of one of the world’s biggest distribution and services companies for independent artists, and they helped give me a new perspective.

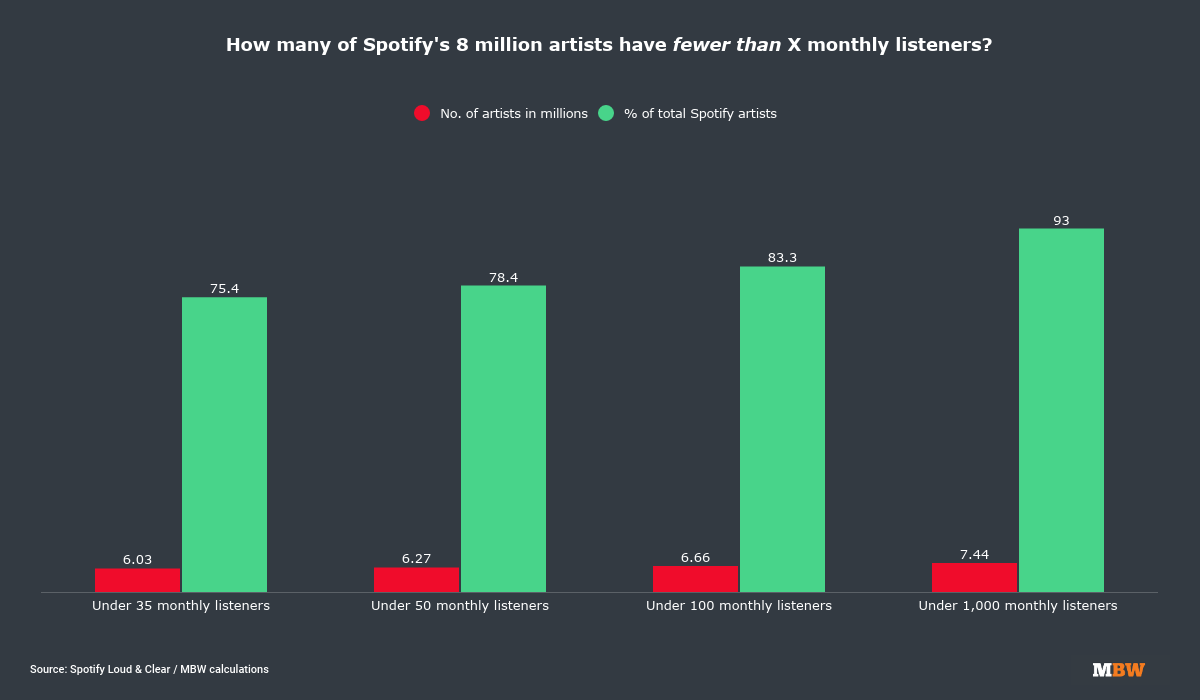

We’re going to have to do a brief calculation here: The actual number of artists on Spotify, at the end of 2021, with fewer than 50 monthly listeners was, according to my calculations, 6.3 million.

Now let’s assume for the sake of this podcast that all of these monthly listeners across all of those 6.3 million artists are unique, [so] didn’t listen to any of the other artists in the 6.3 million group. (This is not a crazy idea in the grand scheme of things. Remember, each of these artists is by nature, statistically unpopular. The idea that you’d listen to two of them in a single session or a single month would be logically quite unlikely.)

For argument’s sake, let’s split the difference and assume that each of these artists (who have under 50 monthly listeners) has an average of 25 monthly listeners: that’s 6.3 million artists, all with a rather measly-looking 25 unique listeners each month on Spotify.

Combined, these artists would therefore have a total of 157.5 million monthly listeners. And this number is really quite significant in the context of a threat to the major record companies.

If you look at the list of the biggest artists in the world today on Spotify, you will find Ed Sheeran at the top, just ahead of Justin Bieber and The Weekend. And currently Ed Sheeran has 83.6 million monthly listeners on Spotify.

That’s roughly half the size of the estimated cumulative listening base of our 6.3 million artists with fewer than 50 monthly listeners each (157.5m).

To put it in much simpler terms: unpopular artists on Spotify, in the grand scheme of things, are commercially irrelevant as individuals. But combined, they are a powerful force.

Getting back to the topic of this podcast, all of this is really not good news for the major record companies. We know that according to Daniel Ekaround 60,000 tracks were being uploaded to Spotify daily in Q1 last year. Some say that number is growing exponentially – it could be up to 70,000 or even 80,000 as time moves on.

This phenomenon cannot help but eat into the major record companies’ market share on streaming services, because those major record companies simply aren’t distributing the majority of these tracks.

Think about what that is doing to the actual number of plays on Spotify. We’ve already suggested that verifiably unpopular artists on Spotify – those 6.3 million – are cumulatively drawing more streams than Ed Sheeran and The Weeknd globally.

So what happens when you also count independent artists with let’s say, between 1,000 and a million monthly listeners on Spotify – and the fact that there’s a heck of a lot of them?

What happens to the major labels’ market share, then?

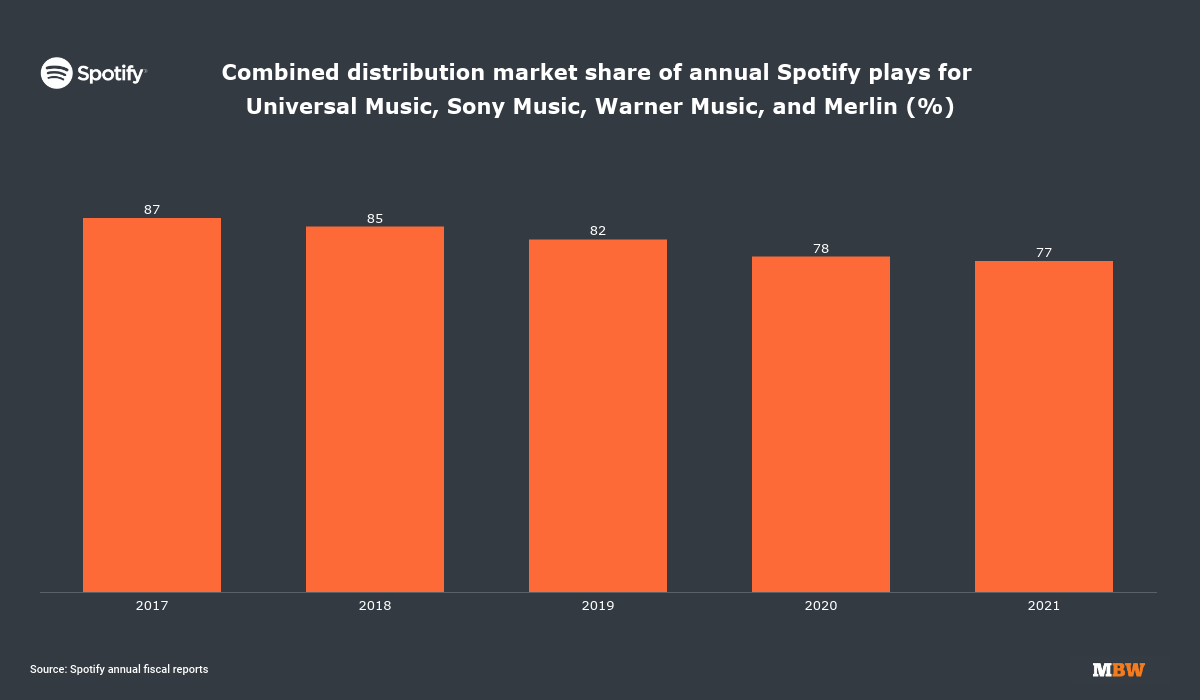

We already know the answer to this question. Spotify in its annual financial report puts a number on the percentage of streams of recorded music that’s distributed by the three major record companies plus Merlin (the three majors: Universal Music, Sony Music and Warner Music).

This number has been falling substantially, although the decline actually slowed slightly last year.

Still, in 2017, these four entities – the majors plus Merlin – claimed 87% of all Spotify streams. Last year, in 2021, these four groups claimed a cumulative total of 77%.

That’s 10% of global streaming market share on Spotify lost by the majors (plus Merlin) in just four years. Alarm bells have got to be ringing about these statistics.

At this point, it’s interesting to bring in the comments of Rob Stringer, the Chairman of Sony Music Group, who was quizzed on streaming market share by an analyst on a Sony financial presentation last week.

Stringer pointed to the trend of these vast oceans of music being released by independent artists on streaming services each day, and how Sony Music has developed a sort of defensive strategy, if you like, of distributing as much of this music as it can while maintaining a threshold of quality in the marketplace.

In other words, Sony will distribute quality music released by independent labels via The Orchard, and it will distribute quality music by independent artists via AWAL, which it acquired last year. But Sony isn’t in business with – as Rob Stringer puts it – “flotsam and jetsam”.

I guess he’s talking about the kind of unpopular music that attracts less than 50 monthly listeners.

Let’s listen to Rob Stringer’s comments from last week here before we analyze them more fully.

[Rob Stringer]: “If there are 80,000 tracks a day being uploaded on major DSPs, then [major label] market share is going to be diluted by default.

“The reason we have a strong strategy in The Orchard and [via] our recent acquisition of AWAL is to take a proportion of that 80,000 – [to] have a bigger proportion of the net that’s being cast for content.

“We realize we have to cast our nets [and] somehow get that music in our ecosystem. Because otherwise, literally, market share will be diluted by default of the sheer volume of tracks [being released].”

Rob Stringer, speaking last week

“[There are] 27,000 labels being distributed by The Orchard globally. So, at the scale end, we realize we have to cast our nets deeper and deeper and somehow get that music in our ecosystem.

“Because otherwise, literally, market share will be diluted by default of the sheer volume of tracks [being released] – even, quite frankly, if [some of that music] is literally like flotsam and jetsam, and it’s just stuff that’s taking up some of the market share because of scale.” [Rob Stringer ends]

For the major record companies, their dominance of streaming market share isn’t just important in terms of their revenues. Crucially, it also affects their leverage when they’re renegotiating licensing agreements with Spotify or Apple or Amazon and other music streaming platforms or owners.

The smaller the majors’ cumulative market share as they go into these licensing negotiations every few years, the less power they have. And the continued gradual erosion of the majors’ market share in the future looks inevitable when you digest the data.

(We’re not even taking into account here by the way, whether Spotify is actually commercially incentivized to drive listeners to non-major label music in order to deliberately weaken the majors’ negotiating ability in those licensing discussions).

Rob Stringer says that Sony currently distributes music from 27,000 independent labels through The Orchard – and that’s a stat with real punch. Then there are an additional clutch of independent artists – perhaps tens of thousands, likely hundreds of thousands – who also go through AWAL.

“Those services who do let anyone upload anything to Spotify et al are building immense scale. Take DistroKid, for example: it claims that it distributes between 30% and 40% of all new music today by volume.”

But both of these services – The Orchard and AWAL are invite-only; artists or labels can’t just decide to upload music through these platforms and automatically get their records on streaming services… they have to be chosen and approved first.

We’ve just seen Universal Music Group mirror this model by pivoting away from DIY distribution with its AWAL rival, Spinnup. You now can’t just upload music via Spinnup and see it on Spotify; you have to be accepted [by UMG] as being of a certain quality first.

Meanwhile, those services who do let anyone upload anything to Spotify et al are building immense scale. Take DistroKid, for example. According to its press materials, DistroKid currently distributes music for over 2 million artists – and it claims that it distributes between 30% and 40% of all new music today.

Yes: DistroKid pretty much claims that it is distributing, by volume, over a third of all new music today.

None of the major record companies can compete with that vastness of volume. And that vastness of volume is inevitably going to keep driving down the majors’ market share on the likes of Spotify.

Even if much of DistroKid’s music is ‘flotsam and jetsam’ – I don’t know if it is or not, but let’s just say for argument’s sake that it is – every single listener that that ‘flotsam and jetsam’ attracts on Spotify and other services is a wound in a major record company’s mission to maintain immense market share dominance of streaming.

So how can we expect the majors to fight back against this powerful tide? Because they surely will?

In Spotify’s model as it exists today, every piece of recorded music in the world is worth the same. It doesn’t matter if we’re talking about Bohemian Rhapsody, 99 Problems, some tuneless dirge I just knocked up on an acoustic guitar, or a large man doing an elongated burp.

If you play it for more than 30 seconds, it gets the same amount of royalty payment as any other track on Spotify that month.

I expect the major labels to take strong issue with this fact soon enough, because right now they’re in a bind. On the one hand, as Rob Stringer explains, they’re trying to play a bit of the volume game and get into bed with as much quality music as possible. But on the other hand, they’re refusing to open their gates to the “flotsam and jetsam”.

“In Spotify’s model as it exists today, every piece of recorded music in the world is worth the same. It doesn’t matter if we’re talking about Bohemian Rhapsody, 99 Problems, some tuneless dirge I just knocked up on an acoustic guitar, or a large man doing an elongated burp.”

The quality threshold remains all-important at the majors.

This business model can only triumph long term if streaming companies start acknowledging that quality music – and we’ll get into what that might mean soon – is deserving of a higher rate of royalty payment than ‘flotsam and jetsam’.

In other words, will Spotify agree that not all music is worth the same, or that a play of Bohemian Rhapsody is intrinsically worth more than a play of a large man’s elongated burp?

Defining the parameters of what constitutes ‘premium’ music versus ‘flotsam and jetsam’ is going to be fun. Music by its nature is subjective. You might think a certain track or an album is complete dreck; I might think it’s celestial, and vice versa. That’s part of what makes the industry so much fun.

But I suspect the majors may at least start asking the following questions of Spotify in future licensing negotiations.

How many subscribers were drawn to your service because of the superstars we licensed to you?

How many people decided to pay for Spotify because of Dua Lipa, or Eminem, or Ed Sheeran, or Bad Bunny, etc?

In that respect, aren’t these artists and their music the most powerful audience acquisition tools at your disposal?

Is there data that supports the idea that established stars – not ‘flotsam and jetsam’ – more powerfully influenced people to pay Spotify money every month for the rest of their lives?

And therefore doesn’t the music of these established stars deserve to recruit a premium versus your average Joe with fewer than 50 monthly listeners?

There is no reason technology like this won’t soon be able to create millions of tracks per day at the touch of a button, and then upload all of them to Spotify within seconds.

Imagine the threat that kind of tidal wave of music hitting services daily brings to the major record companies and their need to dominate market share on Spotify and other platforms.

If the majors are going to take the argument to Spotify that some music simply deserves more financial respect than other music, surely they are now compelled to do so sooner rather than later.